Top 3 Recommended Policies

Ohio’s HVAC contractors keep homes and businesses running through freezing winters and humid summers, making their work essential year-round. But with constant demand comes a steady stream of risks, from equipment damage to employee injuries and liability claims. Having the right insurance coverage is what keeps your business financially secure and compliant with state requirements. This guide explains how HVAC contractor insurance in Ohio works, what types of policies are most important, and how market changes are influencing costs. With the industry continuing to expand and repair expenses on the rise, understanding your coverage options will help you protect your operation, serve your customers with confidence, and maintain your reputation across a competitive market.

Why HVAC Contractor Insurance is Essential in Ohio

Insurance for HVAC contractors in Ohio is not just a regulatory formality—it is a critical business safeguard. HVAC work involves a variety of risks, including property damage, bodily injury, and workplace accidents. Without proper insurance, contractors could face devastating financial losses from lawsuits or claims.

General liability insurance is a foundational coverage that protects against third-party claims of injury or property damage. In Ohio, typical premiums for HVAC liability insurance range between 1.3% and 2.6% of annual gross revenue, making it a manageable but essential expense for contractors seeking to mitigate risk. This statistic, provided by ContractorNerd, highlights the relative affordability of liability insurance compared to the potential costs of litigation or settlements.

Additionally, workers' compensation insurance is mandatory for most Ohio businesses with employees. HVAC contractors typically pay around $2,120 per $100,000 of payroll for this coverage, according to ContractorNerd. This insurance covers medical expenses and lost wages for employees injured on the job, which is particularly important in a physically demanding trade like HVAC installation and repair.

Moreover, HVAC contractors in Ohio should also consider obtaining commercial auto insurance, especially if they use vehicles for transporting equipment and employees. This type of insurance protects against accidents that may occur while driving for work purposes, covering both property damage and medical expenses resulting from vehicular incidents. Given the unpredictable nature of Ohio's weather, which can lead to hazardous driving conditions, having commercial auto insurance is a prudent step for contractors who rely on their vehicles for daily operations.

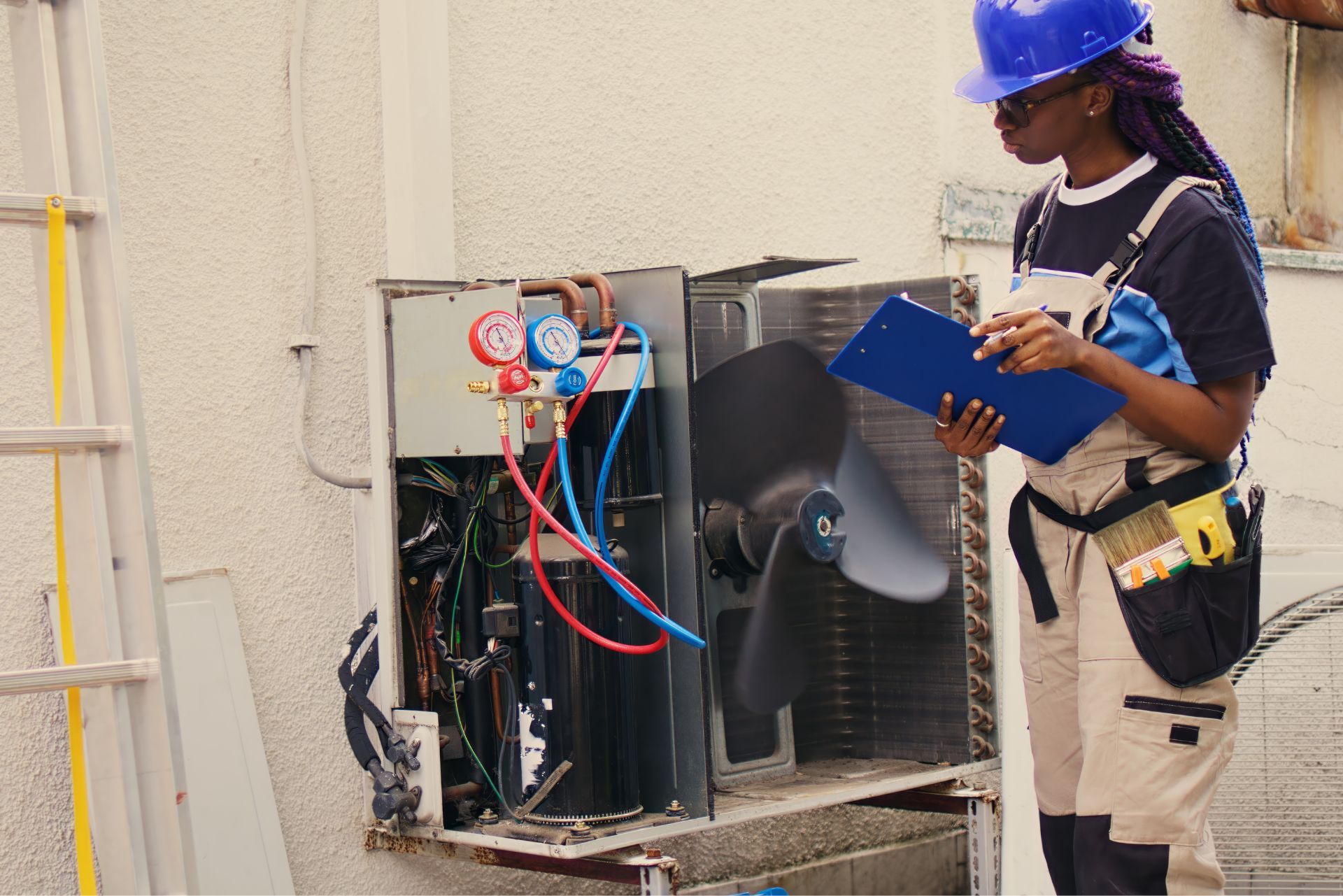

Another vital coverage to consider is equipment and tools insurance, which protects against theft, loss, or damage to the specialized tools and machinery that HVAC contractors use. This type of insurance can be particularly beneficial in a field where the cost of equipment can be substantial. The financial burden of replacing essential tools can be overwhelming, especially for small businesses, making this coverage a smart investment for ensuring operational continuity and minimizing downtime in service delivery.

Types of Insurance Every Ohio HVAC Contractor Should Consider

General Liability Insurance

General liability insurance protects HVAC contractors from claims related to bodily injury, property damage, and personal injury caused by their business operations. For example, if a contractor accidentally damages a customer’s property during installation, this insurance can cover repair costs and legal fees.

Given the nature of HVAC work, where contractors frequently enter clients’ homes and businesses, this coverage is indispensable. The premium range of 1.3% to 2.6% of gross revenue makes it a cost-effective way to shield the business from significant financial exposure. Additionally, general liability insurance can also cover incidents that occur off-site, such as during a consultation or while picking up supplies. This broad coverage ensures that contractors are protected against a variety of unforeseen circumstances that could otherwise jeopardize their financial stability.

Workers' Compensation Insurance

HVAC contractors in Ohio must comply with state laws requiring workers' compensation insurance if they have employees. This insurance covers medical treatment and lost wages for workers injured while performing their duties. HVAC work involves risks such as electrical hazards, falls, and heavy lifting, making workers' comp coverage a vital safety net.

Ohio HVAC contractors typically pay about $2,120 per $100,000 of payroll for workers’ compensation. This cost reflects the inherent risks in the trade and underscores the importance of maintaining a safe work environment to potentially reduce premiums. Moreover, investing in safety training and equipment can not only minimize accidents but may also lead to lower insurance costs over time, creating a win-win scenario for both the employees and the business.

Commercial Auto Insurance

Many HVAC contractors rely on vehicles to transport tools, equipment, and personnel. Commercial auto insurance covers vehicles used for business purposes, protecting against accidents, theft, and damage. Without this coverage, contractors could face out-of-pocket expenses for vehicle repairs or liability claims arising from accidents.

In addition to protecting the vehicles themselves, commercial auto insurance can also cover medical expenses for injuries sustained in an accident involving a business vehicle. This is particularly important for HVAC contractors who may be on the road frequently, traveling between job sites. Furthermore, some policies can also provide coverage for equipment that is damaged while in transit, ensuring that contractors are not left financially vulnerable if an accident occurs.

Equipment and Tool Insurance

HVAC contractors invest heavily in specialized tools and equipment. Insurance policies that cover theft, loss, or damage to these assets help ensure that contractors can quickly replace essential items without disrupting business operations.

Additionally, equipment and tool insurance can cover the costs associated with renting replacement tools while waiting for repairs or replacements, which can be crucial for maintaining workflow. Given the high cost of HVAC equipment, having this insurance not only protects the contractor's investment but also ensures that they can continue to meet client demands without significant delays. This type of insurance can also be tailored to cover specific high-value items, providing peace of mind for contractors who rely on advanced technology to deliver quality service.

Surety Bonds

While not traditional insurance, surety bonds are often required for HVAC contractors bidding on public projects or seeking certain licenses. Bonds guarantee that contractors will fulfill their contractual obligations, providing clients with financial protection if the contractor fails to deliver.

Surety bonds serve as a testament to the contractor's reliability and professionalism, often giving potential clients added confidence in their ability to complete projects on time and within budget. In many cases, the bond amount is based on the total value of the contract, and obtaining one can also enhance a contractor's reputation in the industry. Furthermore, maintaining a good standing with surety companies can lead to better rates and terms for future bonding needs, making it a strategic investment for long-term business growth.

How Rising Repair Costs and Customer Preferences Impact Insurance Needs

The HVAC industry in Ohio is experiencing notable shifts due to rising repair costs and changing consumer behavior. Home warranty companies in Ohio have seen a surge in demand as homeowners seek financial safeguards against unpredictable home repair expenses. An industry analyst notes that “a home warranty serves as a financial safeguard against the unpredictability of homeownership,” reflecting a growing trend toward risk mitigation in home services. This increase in demand for home warranties is not just a response to rising costs; it also indicates a broader shift in how homeowners perceive the value of their investments in home systems and appliances.

This trend impacts HVAC contractors because customers increasingly expect reliable service and may prefer companies with strong reputations and insurance coverage that ensures accountability. In fact, a survey highlighted by ACHR News found that homeowners often choose HVAC contractors based on past experiences and word-of-mouth recommendations. This makes having proper insurance not only a risk management tool but also a marketing asset that builds trust with clients. Furthermore, as homeowners become more educated about their options, they are more likely to inquire about the specific types of insurance coverage a contractor holds, including liability and workers’ compensation, which can significantly influence their decision-making process.

Contractors who maintain comprehensive insurance coverage demonstrate professionalism and reliability, which can differentiate them in a competitive market where customers value peace of mind as much as price. Additionally, the rise of online reviews and social media platforms has amplified the importance of reputation management. A single negative review regarding a contractor's reliability or service quality can deter potential customers, making it crucial for HVAC professionals to not only provide excellent service but also to ensure they are protected against potential liabilities. As consumer preferences evolve, HVAC contractors must adapt by not only enhancing their service offerings but also by actively promoting their insurance coverage as a testament to their commitment to quality and customer satisfaction.

Insurance Challenges Specific to Ohio HVAC Contractors

Ohio’s geographic location in the Midwest exposes HVAC contractors to unique insurance challenges. Insurers are increasing wind and hail deductibles to cope with rising claims from medium-sized storms, as reported by Crain’s Cleveland Business. These weather-related risks can affect both contractors’ property and vehicles, as well as the homes they service.

Contractors should carefully review their policies to ensure adequate coverage against weather-related damages and consider endorsements or additional policies if necessary. Understanding these regional risks helps contractors avoid unexpected out-of-pocket expenses after storm damage or other natural events.

Moreover, with the HVAC industry in Ohio growing rapidly, contractors face increased competition and operational complexities. Balancing insurance costs with comprehensive coverage requires strategic planning and consultation with knowledgeable insurance providers familiar with the HVAC trade and Ohio’s market conditions.

In addition to weather-related risks, Ohio HVAC contractors must navigate the complexities of regulatory compliance, which can vary significantly from one municipality to another. Local building codes, licensing requirements, and safety regulations can create a patchwork of obligations that contractors must adhere to, adding another layer of risk. Failure to comply with these regulations not only jeopardizes their business operations but can also lead to costly fines and increased insurance premiums.

Furthermore, the rise of technology in the HVAC sector, including smart home systems and energy-efficient installations, presents both opportunities and challenges for contractors. As they adopt new technologies, they must also consider the implications for their insurance coverage. For instance, specialized equipment may require additional coverage or endorsements, and the liability associated with installing advanced systems can increase the complexity of their insurance needs. Staying informed about these developments is crucial for contractors to mitigate risks and ensure that their insurance policies evolve alongside their business practices.

Tips for Choosing the Right Insurance for Your HVAC Business

Selecting the right insurance policies involves assessing your business size, scope of work, and risk exposure. Here are some practical tips for Ohio HVAC contractors:

- Evaluate Your Risks: Consider the types of projects you undertake, the number of employees, and the value of your equipment. This will guide you in choosing appropriate coverage limits.

- Compare Multiple Quotes: Insurance premiums can vary significantly. Obtain quotes from several providers to find competitive rates without sacrificing coverage quality.

- Work With Specialized Insurers: Choose insurance companies or brokers experienced in serving HVAC contractors to ensure policies address industry-specific risks.

- Review Policy Details: Understand exclusions, deductibles, and coverage limits. For example, check how wind and hail deductibles might affect your claims in Ohio’s climate.

- Maintain a Strong Safety Program: Implementing workplace safety measures can reduce workers’ compensation claims and potentially lower premiums.

- Leverage Customer Trust: Promote your insurance coverage as part of your commitment to quality and reliability, reinforcing word-of-mouth referrals that are crucial for business growth.

In addition to these tips, consider the importance of understanding the nuances of different types of coverage available to you. For instance, general liability insurance protects against third-party claims for bodily injury or property damage, which is essential in an industry where accidents can happen. On the other hand, equipment breakdown insurance can cover the repair or replacement of essential tools and machinery, ensuring that your operations can continue with minimal disruption. As HVAC technology evolves, staying informed about new risks and corresponding insurance options can provide an added layer of security for your business.

Furthermore, networking with other HVAC professionals can be invaluable when it comes to insurance insights. Joining local trade associations or attending industry conferences can provide opportunities to learn from peers about their experiences with different insurers and policies. These interactions can also lead to recommendations for reputable brokers who understand the unique challenges faced by HVAC contractors in Ohio. By fostering relationships within the industry, you can gain a wealth of knowledge that can help you make informed decisions about your insurance needs.

Conclusion: Protecting Your HVAC Business in Ohio

Insurance is a vital component of running a successful HVAC contracting business in Ohio. With industry growth expected to reach billions in revenue and increasing customer demand for dependable service, contractors must prioritize comprehensive insurance coverage to manage risks effectively.

From general liability to workers’ compensation and specialized coverages, the right insurance policies not only protect your business assets but also enhance your reputation among clients. Given the rising repair costs and evolving market dynamics, staying informed about insurance trends and regional challenges is essential.

Ohio HVAC contractors are encouraged to consult with experienced insurance professionals and regularly review their coverage to adapt to changing risks. Doing so ensures that when unexpected events occur, your business remains resilient and ready to serve your customers with confidence.

For further insights into HVAC insurance and industry trends, explore resources such as

ContractorNerd’s HVAC insurance guide and the

ACHR News survey on homeowner preferences.

Contact Us

HVACInsure is fully licensed and permitted to sell contractor and commercial insurance in Ohio.

We proudly serve clients throughout Ohio and maintain partnerships with local Ohio insurance carriers to ensure HVAC professionals receive compliant, affordable, and comprehensive coverage that meets project and regulatory requirements.

HVACInsure Focuses on Ohio HVAC Contractor Insurance

Columbus – Cleveland – Cincinnati – Toledo – Akron – Dayton – Parma – Canton – Youngstown – Lorain – Hamilton – Springfield – Kettering – Elyria – Lakewood – Cuyahoga Falls – Middletown – Euclid – Newark – Mansfield – Mentor – Beavercreek – Cleveland Heights – Strongsville – Dublin

Frequently Asked Question

Common HVAC Contractor Insurance Questions in Ohio

These FAQs address common contractor questions. As HVACInsure grows, we will update this section with real client experiences and answers.

How does Ohio's manufacturing economy affect my HVAC insurance?

Ohio's industrial base needs HVAC contractors. We cover plant maintenance, process cooling, and the specialized requirements of manufacturing work.

What coverage do I need for Cleveland, Columbus, and Cincinnati commercial work?

Ohio's cities have active commercial markets. We cover the liability exposure and certificate requirements of urban commercial projects.

Do I need special coverage for Ohio's Lake Erie climate?

Lake effect weather creates unique challenges. We cover the humidity, rapid temperature changes, and emergency demands of northern Ohio.

What about coverage for Ohio's many older buildings?

Ohio cities have significant older building stock. We cover the liability of retrofitting HVAC in properties with code challenges.

How do Ohio's licensing requirements affect my insurance?

Ohio HVAC licensing varies by jurisdiction. We help you meet local requirements across your service area.

Can I get coverage for work across Ohio's diverse regions?

Absolutely. Ohio varies from Appalachian hills to Great Lakes climate. We structure coverage for your actual service area.

Still have questions?

Can’t find the answer you’re looking for? Please chat to our friendly team!

About The Author: James Jenkins

I’m James Jenkins, Founder and CEO of HVACInsure. I work with HVAC contractors and related trades to simplify insurance and make coverage easier to understand. Every day, I help business owners secure reliable protection, issue certificates quickly, and stay compliant so their teams can keep working safely and confidently.

Recognized by National HVAC Trade Associations

These trusted organizations set best practices and standards that carriers rely on when underwriting HVAC risks.

Membership signifies adherence to HVAC industry standards and contractor best practices.